“Ninety percent of all millionaires become so through owning real estate. More money has been made in real estate than in all industrial investments combined. The wise young man or wage earner of today invests his money in real estate.”- Andrew Carnegie

Property does, more often than not, make tremendous wealth for the higher echelons of society. Indeed, I recall not too long ago, discussing the trends facing society with a friend who was absolutely bearish on the property (around 2009). The discussion centered around the collapsing market, and ultimately, the conclusion I came to, although he was less than convinced, was there was so much wealth stored in real-estate and land, that the market was “invictus” as far as collapsing was concerned. That was certainly true of property back then. Property has rallied since 2009, more or less globally. I am, however, decidedly bearish on property today- I’ll explain why.

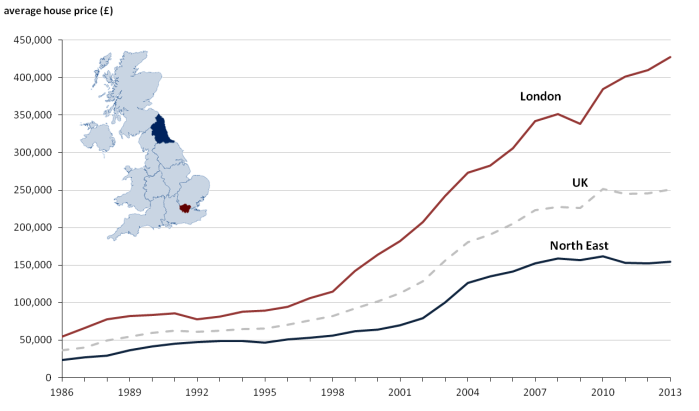

Markets have been rallying (more or less) globally:

This is especially true of Canada, Australia and China (and the City of London), where they property values hardly stumbled after the 2009 Subprime Mortgage Crisis in the US. It is also true of the US and the UK (outside London) to a lesser extent, which declined, bounced and are now slowing again.

I’ve talked substantially about the general risk factors facing property here. So, for the rest of this article I will focus specifically on one form of property investment: crowdfunded buy-to-rent property.

What is crowdfunded buy-to-rent property?

The principle is quite simple for anyone who is familiar with websites like Kickstarter or CrowdCube– many individual investors pool their money together to fund an investment on a smaller scale to afford a larger investment. In the case of buy-to-rent, it is a house, which will then be purchased and let out to a young couple, or a family, or business professionals and so on.

Real world example:

So, taking a real world example of how the investment would work (see: here). The information is as follows:

Investment capital (total): 861200 (GBP)

Number of Shares: 1000000

Share price: 0.8612 (GBP)

If we placed the maximum purchase order we could, 50000 GBP. An initial 2% fee would be extracted up front, leaving approximately 49000 investment capital. This is 56897 shares, or approximately 5.7% (5.6897% to be precise) ownership stake in the property.

The rent paid out on the property is estimated to be 27962 GBP per year, after subtracting costs and a 10.5% fee. The share of the dividend yielded with our 56897 shares would be 1567.90 GBP over 12 months, approximately 3.18% dividend yield. Assuming full occupancy, and no late rental payments (or declining rental values) this figure should be fixed for at least 2 years based on the mortgage schedule.

Now, there are two components to the investment to consider: the market value of the house, and the dividends (paid out from the rent) every time period. Thus, a decline in house price OR a decline in rental value will affect the future value of the investment.

Risk factors affecting this investment:

There are many risk factors affecting this investment, indeed, it is almost as complex as equity investment. The risks are a combination of general systematic (market) risks, risks facing tenancy issues, risk facing legal issues, as well as risks involved with the business. I’ll take each in turn.

Systematic risk:

This includes factors (many of which are related) like interest rate risk, capital flight, recessionary risk, population decline, stagnating real wages, increased property taxes and so on.

Specific risk:

This includes factors like local property value trends, risks related to the tenants, and risk of property damage.

Other risks:

There is, of couse a risk of the business who operates the crowd-funding platform going bankrupt. There’s counterparty risk involved. Risk of changing legal requirements etc.

It is also worth mentioning that there is a legal framework for capital gains on dividends within the UK which all investors must adhere to. This will further eat into profitability past a certain point.

Reward is important, but understanding and foreseeing the risks involved in this sort of investment arrangement is critical. Reward should be sought, but risk should be avoided, or hedged against.

Overall opinion of the investment:

As someone who is not already on the property ladder, this investment makes zero sense on a fundamental level. This is because the company that you are contracting with is in the process of purchasing up the very properties you would (as a first time buyer) be eligible to rent, and thus, elevating property prices.

However, caution is advised in digesting this logic, the trend is rarely logical and in this case, herding really does count. Therefore, if an entire generation of first-time buyers are intent on pushing property prices to breaking point (and then some) by investing in “investment schemes” like this, it may be worth getting ahead of the crowd and investing in the trend, rather than sitting out and watching property skyrocket with no dividends. I’ll leave that for the reader to decide- fight against the market trend at your peril.

This type of investment is probably best suited for those who are no longer paying off a mortgage on their home, and want a stable investment without managing the headaches of tenancy, legal fees and the general headaches associated with being a landlord.

Edit: Additional details on the types of risks facing this sort of investment can be obtained upon request via the email listed in this blog.

{kind=link}